Just about anyone can cover one single spot. Maybe you start with a Google Grant, helping drive traffic to your site. Simple. Manageable.

Then you stretch a little further, supplementing with paid search. You spot an opportunity to reach new audiences on Instagram, and soon enough you are straining to include several social media platforms.

Before you know it, you are knee-deep in display ads, you’ve got your hands on pre-roll video, you’ve elbowed your way into an experiment with digital audio, and you’re pretzeling audaciously to cover connected TV, bending over backward to find and engage the audiences that matter to your cause.

Above all else, it takes flexibility to manage the array of channels, platforms, creative, audiences, budgets, and response metrics that make up a modern ads program. In order to try to capture more of this complexity, we are including advertising investment data from non-digital channels for the first time in M+R Benchmarks this year. We’ll put a spotlight on digital ad performance a little later, but first let’s look at how nonprofits approached advertising overall.

Including both digital and non-digital channels, 61% of advertising spending by nonprofits was dedicated to direct fundraising efforts. Awareness advertising accounted for 25% of spending, and nonprofits spent 10% of advertising dollars on lead generation.

The balance between these three was markedly different for nonprofits of different sizes. Small nonprofits spent 89% of budgets on direct fundraising, and only 3% on awareness advertising. For large nonprofits, the split was 58% direct fundraising, 27% awareness. With larger budgets comes greater flexibility to invest in branding, education, and expanded reach.

Next, let’s look at spending by channel for each of these three major advertising goals. Among digital channels, search and social media spending combined made up 80% of fundraising advertising budgets.

Large nonprofits tended to spread spending more widely into other channels. Search and social accounted for 90% of spending by small nonprofits, 80% for medium nonprofits, and 78% for large nonprofits. Larger advertising budgets create more opportunity to experiment and optimize within new channels.

Among non-digital channels, linear television consumed the majority of fundraising advertising budgets — 77% overall. Small nonprofits devoted 42% of non-digital fundraising advertising budgets to print, compared to just 20% for medium nonprofits and 17% for large nonprofits.

The balance between channels looks quite different for advocacy advertising, where the immediate goal is to drive signatures or some other action rather than donations. Among digital channels, social advertising made up half of advocacy spending — 50% overall, and 100% of spending by small nonprofits.

Compared to fundraising advertising, non-digital spending investments were not as heavily skewed toward linear television. Large nonprofits spent 16% of non-digital advertising budgets on print, and 15% on out of home advertising — billboards, bus shelter ads, etc. Medium nonprofits split this spending between linear television (63%) and print (37%). Small nonprofits did not report meaningful spending on non-digital advocacy campaigns.

For awareness advertising, nonprofits of all sizes shifted spending toward digital video (18% on average overall), out of home, and radio advertising. When nonprofits were looking to raise visibility to wider audiences rather than drive direct response, these channels were more important.

Total investment in advertising increased by an average of 13% in 2023, with some sectors reporting a significant increase in ad spending (Environmental: up 35%; Health: up 33%) and others scaling back (Public Media: down 17%; Rights: down 9%).

Small nonprofits increased ad spending by 27%, medium nonprofits by 22%, and large nonprofits by 11%.

Nonprofits increased fundraising ad spending across nearly every channel. The biggest spike in spending was in radio advertising (as we’ve seen, radio made up only a small share of overall budgets, so this is a large percentage change but not necessarily a big shift in absolute dollar amount). Connected TV increased the most among digital channels, with 50% larger budgets on average. The only fundraising channel where nonprofits pulled back on spending compared to 2022 was Meta.

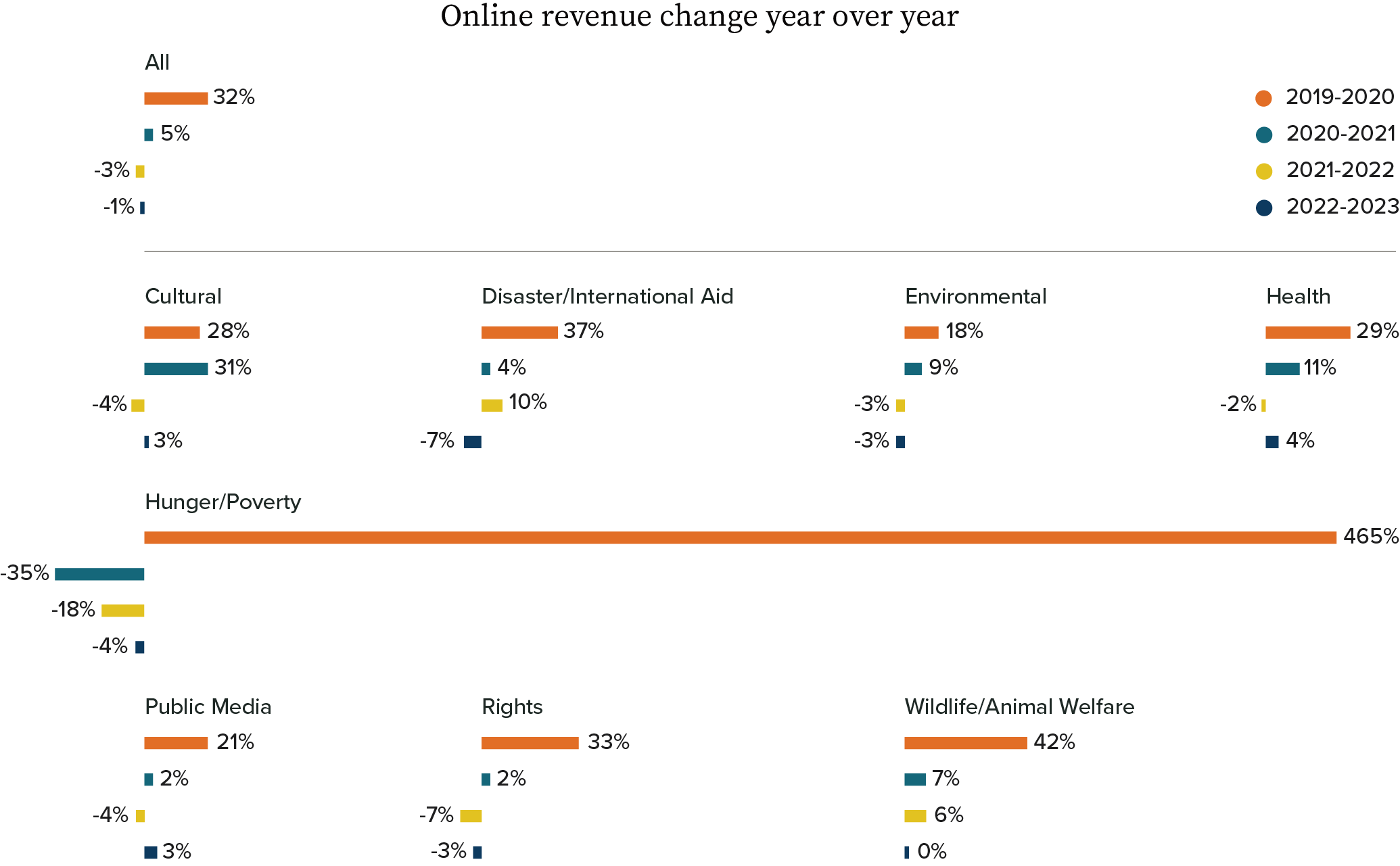

Now let’s turn our attention specifically to digital channels. To put these year-over-year changes in perspective, nonprofits reinvested $0.12 in digital advertising for every dollar raised online. As with the change in spending levels, we see large differences by sector.

In the Health sector, a nonprofit with $100,000 in online revenue would spend $23,000 on digital advertising over the course of the year. A Rights nonprofit with $100,000 in online revenue would invest just $3,000.

We’ve examined ways nonprofits stretch, balance, and redirect advertising budgets. Now we can take a look at how audiences responded, starting with return on ad spend (ROAS) for fundraising advertising.

As we mentioned earlier, and as we mention in every year’s M+R Benchmarks, search advertising has the highest ROAS of any channel. For every $1.00 nonprofits spent on search advertising for fundraising, they raised $2.70 in revenue.

Occasionally as we are analyzing M+R Benchmarks data, we see results that knock us off balance. While we don’t make direct comparisons from one edition of M+R Benchmarks to the next, we take notice when a data point is far out of step with what we typically see. Return on ad spend for display advertising was one of those this year — the $1.26 raised per dollar spent is much higher than what we have reported in previous years.

We give these metrics extra scrutiny beyond our typical QA to make sure we haven’t made an error in our calculations. If the numbers hold up, we look for possible explanations, even if it means getting tangled up in knots. The display ROAS numbers held up.

So what’s going on? We can speculate.

As we get closer to Google Chrome deprecating support for third-party cookies, nonprofits have adopted more sophisticated cookieless measurement tools. This in turn may enable them to better track viewthrough conversions from Safari and Firefox, allowing more revenue to be correctly attributed to display advertising.

Another (possibly smaller) factor: Google has strongly encouraged advertisers to use campaign formats that combine multiple channels. For example, Performance Max campaigns set audience and performance goals, with Google serving a mix of Google Display Network, YouTube, and search advertising. Because these campaigns include search placements, they often have a high ROAS, which can be difficult to distinguish from display-only campaigns.

Among non-digital channels, the highest ROAS was $0.56 for radio. Out of home had the lowest ROAS, with nonprofits seeing just $0.03 in revenue per dollar spent on out of home fundraising advertising.

Cost per donation has a major impact on ROAS — the more it costs to generate a single gift, the more difficult it is to see a positive return. Search had a high ROAS, and we see a relatively low cost per donation of $55. Out of home has a low ROAS, and we see an actually very high cost per donation of $2,622.

Our data set doesn’t allow us to make ROAS comparisons between nonprofit sectors or sizes for most channels, but we are able to do so for three digital channels: display, search, and Meta.

Across nonprofits of every size and sector, search advertising had the highest return on ad spend. Hunger/Poverty nonprofits saw the best ROAS of any sector across all three channels. The Hunger/Poverty sector’s $4.52 ROAS for display advertising was by far the highest of any sector, and suggests that nonprofits in this space could increase spending significantly while maintaining positive results.

Cost per donation was highest in all channels for small nonprofits. Larger budgets can create more opportunities for testing and optimization, which may have allowed large nonprofits to bring down the average cost per donation. Rights nonprofits spent more than those in any other sector to generate a gift in display and search, though this did not hold true on Meta.

Choosing how to balance advertising budgets depends on metrics like cost per donation and ROAS, along with a complex, overlapping web of considerations. With a low cost per donation and a high ROAS, nonprofits prioritized search. Out of home advertising was inefficient for direct fundraising, but maintaining a visible presence in specific communities might be important to a nonprofit’s goals. Nonprofits might prioritize reaching specific audiences, or hold back on Twitter/X spending out of concerns about the platform.

Beyond generating an immediate return on spending, nonprofits also used advertising to generate leads, grow email and mobile messaging audiences, and drive web traffic.

The average gift to generate a lead through advertising was $3.33, with a wide range between nonprofits in different sectors. At the low end, Public Media nonprofits spent just $0.49 per advertising lead, while at the high end Hunger/Poverty nonprofits spent $18.18 per lead.

Part of this variance is driven by different levels of investment in advertising platforms. The lowest cost per lead was found with cost-per-acquisition (CPA) buys — these platforms often host advocacy actions that reach a large audience, and allow nonprofits to negotiate a set cost per new subscriber. The average cost per lead for these platforms was $1.31, with large nonprofits spending just $1.08 per lead.

Meta had an average cost per lead of $4.44, with significant variation by sector. TikTok and Google/YouTube efforts had the highest cost per lead.

For some nonprofits, these lead generation efforts were an important part of maintaining a healthy email program. The average ratio of ad-acquired lead to start of year email list size was 0.06. That means that a nonprofit that started 2023 with 100,000 email subscribers would acquire 6,000 new leads via ads over the course of the year.

The median figure for Disaster/International Aid nonprofits was twice as high — a ratio of 0.12, so that nonprofit with 100,000 subscribers on January 1 would add 12,000 new ad-acquired leads. At the 75th percentile, the ratio was 0.47 for Disaster/International Aid nonprofits, the equivalent of adding 47,000 leads to a 100,000 subscriber list over the course of the year. That many new subscribers in a relatively short time can have a dramatic impact on email and mobile messaging performance.

We began this section noting that Google Grants is often the starting place for nonprofits exploring advertising, so let’s end there as well. These placements differ from paid search advertising.

First, they are run with ad credits; we’re presenting Google Grants data in terms of “dollars spent” to put it on similar footing to other channels, but this advertising doesn’t represent actual spending.

Google also imposes caps on total budget and cost per click for Grants ads, limiting the terms nonprofits can cover using Grants. Perhaps the most important difference is that Google Grants search results appear below paid results, which makes users less likely to click.

The upshot of these differences is that Google Grants ads were not nearly as effective as paid search efforts. The ROAS for these Google Grants campaigns was $0.13 overall; the average ROAS for paid search was $2.70. Even though Google Grant placements are free, the net return is still significantly lower than paid search.

The “cost per donation” for Google Grants was also far higher than for paid search. Remember that this “cost” is in ad credits rather than payments made by nonprofits. On average, nonprofits spent the equivalent of $1,192 in Google Grants credits to generate one donation.

While direct fundraising metrics fall short of paid search, Google Grants can make a meaningful impact on digital programs. Nonprofits received 332 site visits for every $1k in Grant spend. Small nonprofits were particularly effective at generating web traffic with Google Grants, with 488 visits per $1,000 spent.

Advertising platforms, audience preferences, and nonprofit strategy are changing quickly. Building a successful program means adapting, adjusting, and stretching to meet those twists and turns.